|

| http://www.cssny.org |

Invited

Testimony

Tom Waters and Victor Bach

Housing

Policy Analysts

Community Service Society ofNew York

Community Service Society of

At Public

Meeting

April

25, 2013

Thank you for the

opportunity to present our concerns about the potential impact of this year’s

RGB decisions on low-income New Yorkers. Rent-regulated

apartments are still the primary source of housing for the city’s 1.1 million low-income[1] households—about

two out of five of these families will be affected by the rent guideline

increases set by this body. Only 18 percent of the city’s low-income rent

stabilized tenants have a Section 8 voucher, leaving more than 336,000 poor and

near-poor households without one. The slow recovery of the city’s economy is

still not producing enough jobs, with dire consequences for these low-income

renters. The unemployment rate remains at 8.9 percent,[2] almost

double its level before the financial crisis of 2007.

Tenant

Experience in the Private Rental Market, Pre- and Post-Recession

The 2011 New York City Housing and Vacancy Survey and

the 2011 American Community Survey, both conducted by the U.S. Bureau of the

Census, are still the most recent sources of statistical information on New York City New York

Chart 2 describes rent and income shifts

experienced by tenants in private unassisted rentals over the three most recent

HVS studies conducted in 2005, 2008, and 2011. Net increases in median rents

over the six-year period vastly outpaced net gains in median incomes for the

typical renter. Overall, rents soared to a net gain of 31 percent over the six

years, compared to an income gain of only 12 percent. The disparity between the

two is a clear indication of rapidly rising rent burdens, the portion of

household income that is paid for rent.

The disparity between rent and income trends is

evident in both rent-regulated and unregulated apartments. Even under regulated

rents, the median contract rent escalated by 26 percent over the six years,

more than twice the 12 percent net increase in median renter income. In

unregulated units, rents increased by 36 percent against an increase in tenant

incomes of 25 percent. Belts tightened for all tenants, regulated and

unregulated, as rent escalation took a larger and larger bite out of household

income, leaving families with less residual income to cover other non-housing

living costs.

The triennial HVS surveys also

confirm the dramatic impact of the recession on renter incomes and their

ability to keep up with rising rents. Median income increases roughly

paralleled rent increases through 2008, a growth period in the local economy,

after which there is post-recession fall-off in household incomes while median

rents continue to escalate.

ALL PRIVATE RENTALS

|

2005

|

2008

|

2011

|

Median Contract Rent

|

$900

|

$1,000

|

$1,176

|

Median Household Income

|

$38,000

|

$44,000

|

$45,000

|

REGULATED RENTALS

|

|||

Median Contract Rent

|

$832

|

$909

|

$1,050

|

Median Household Income

|

$33,700

|

$38,000

|

$38,132

|

UNREGULATED RENTALS

|

|||

Median Contract Rent

|

$1,000

|

$1,200

|

$1,369

|

Median Household Income

|

$44,000

|

$50,200

|

$55,000

|

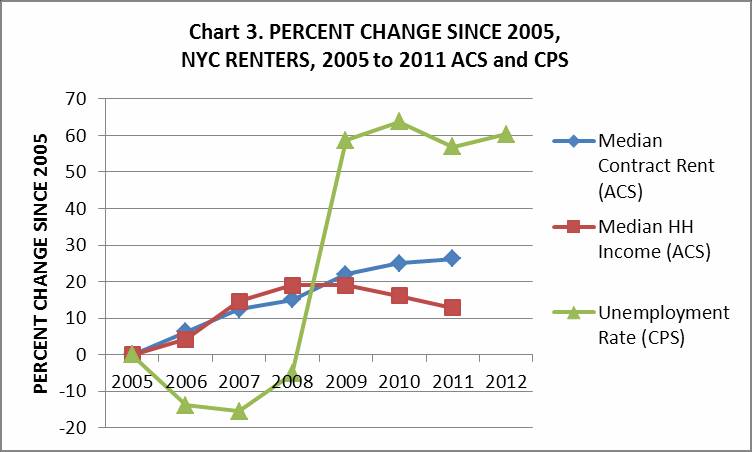

The ACS data provide a clearer

annual picture of rent and renter income trends from 2005 through 2010, which

we compare to city unemployment[3]

in Chart 3. Again, the picture is one of persistently rising median rents

through the six years against median renter incomes that rose through 2008 and

fell off dramatically while the unemployment rate was high from 2009 to 2011.

Unemployment declined from 2005 to 2008 during the

city’s upward economic cycle, then spiked in 2009 and 2010 following the

recession.[4] Per

capita household residual income—the income remaining per member once rent is

paid—is arguably the best proxy for rent-income stresses, because it takes into

account household size. As a whole New York tenants across the rental sectors

experienced a net loss of over 2 percent in residual per capita income

(constant 2010 dollars), largely occurring after 2008. Once the recession

struck, New York

It can be assumed that the picture for renters in

unassisted private apartments, particularly lower-income renters, is bleaker

than the ACS data indicate. ACS data do not distinguish among the range of housing

types that renters occupy, from public housing to private government-subsidized

housing, to private unassisted rentals, both regulated and unregulated. As a

result the ACS renter population includes over 300,000 households who live in

government-assisted housing, where rents are affordable and based on income.

Even so, the ACS data point to a rapid rise in the incidence of high gross rent

burdens (rent plus utilities at 50 percent or more of income) to new highs over

the 5-year period, with a net 3.7 point post-recession increase between 2008

and 2011. (See Chart 4.)

Low-Income Tenants in the Private Rental Market, Pre- and

Post-Recession

The experience of low-income

tenants in the private rental market mirrors that of renters throughout the

city. But because their unemployment rates are roughly double those of renters

as a whole[5],

the impacts on rent-income stresses and residual incomes is much more severe. Chart

5 confirms the extent to which net rent increases over the 6-year period

outpaced income gains. Surprisingly, based on the 2005 starting points, the net

rent increases in regulated units (29 percent) exceeded those in unregulated

apartments (25 percent). By comparison, household incomes increased by from 14

percent.

Residual

per capita incomes declined sharply by 11 percent for low-income renters, but

the impact was far more severe in the unregulated market (21 percent decrease)

than in the regulated market (7 percent decrease). In short, the dynamics of an

escalating local rental market, combined with the post-recession effects on

employment and income, have left low-income renters in far worse economic

circumstances than they were in before the recession.

ALL PRIVATE RENTALS

|

2005

|

2008

|

2011

|

Med. Contract Rent

|

$800

|

$900

|

$1,000

|

Med. Household Income

|

$15,000

|

$16,000

|

$17,160

|

Med. PC Res Inc Mo ($2011)[6]

|

$388

|

$371

|

$346

|

REGULATED RENTALS

|

|||

Med. Contract Rent

|

$750

|

$830

|

$966

|

Med. Household Income

|

$14,000

|

$15,000

|

$16,220

|

Med. PC Res Inc Mo ($2011)

|

$395

|

$377

|

$367

|

UNREGULATED RENTALS

|

|||

Med. Contract Rent

|

$920

|

$1,050

|

$1,150

|

Med. Household Income

|

$16,000

|

$18,000

|

$18,590

|

Med. PC Res Inc Mo ($2011)

|

$408

|

$368

|

$323

|

As a

result, median rent burdens and the incidence of high rent burdens (rent at 50

percent or more – this time not including utilities) among low-income renters

reached a 6-year high as of 2011. (See Chart 6.) Estimates based on the CSS

subsample[7]

indicate a 4-point increase in median rent burdens in both regulated and

unregulated apartments—a rise from 45 to 49 percent in regulated units by 2011,

and from 48 to 51 percent in unregulated units. The growing incidence of high

rent burdens was even more dramatic. By 2011, a majority (51 percent) of

low-income renters in the market were carrying burdens of at least half their

incomes, up from 43 percent in 2005. In the regulated stock, high rent burdens

rose from 45 to 49 percent of low-income families.

Supplemental rent increases

The New York City Rent Guidelines

Board sometimes considers adding extra rent increases for apartments renting

for under $1,000. They added such a supplemental increase last year.

This supplemental increase would

seem to be based on the assumption that a $1,000 rent is excessively low. But

from the point of view of affordability, this is simply not true. In 2010, the

median income for rent-stabilized tenants was $38,000. That means that for half

of the tenants affected by the RGB’s actions, an affordable rent (30 percent of

income) is no more than $950.

The tenants living in the city’s

under-$1,000 rent-stabilized apartments are primarily people who cannot afford

more. Their median income is $28,000, and half of them have incomes below twice

the poverty line (23 percent poor and 29 percent near-poor). More than half of

these tenants (54 percent) live in lower-rent areas of the Bronx, Brooklyn,

Queens, and Staten Island . Just 10 percent

live in Manhattan below Harlem, 13 percent in Upper Manhattan, 8 percent in the

gentrifying areas of Brooklyn and Queens adjacent to Manhattan, and 15 percent

in higher-rent outer-ring neighborhoods such as Flushing or Bay Ridge. Three

quarters of these tenants are people of color: 30 percent black, 38 percent

Latino, and 6 percent Asian. Almost half (47 percent) are in households headed

by an immigrant.

Conclusions

In light of rent escalation trends that persisted

before and since the recession struck the city, it would appear that the

private rental industry has not suffered a decline as a result of the economic

crisis, certainly not a decline comparable to the losses in income and

employment that continue to beset New York renters, particularly low-income

tenants.

Certainly the impacts of a global recession and

financial crisis on the income and employment of New Yorkers, and their ability

to pay for their apartments, are hardly within the control of the city or of

the RGB. However, RGB decisions over recent years have contributed

significantly to the growing rental affordability crisis at this stage of the

presumed recovery. At a time when the RGB should have exercised restraint to

ease the impacts of the recession on its struggling resident constituency, it

has tended to err on the side of owners by granting larger guideline increases

than were necessary.

In recent years, the RGB has overestimated

projected operating costs compared to the actual cost increases later reported

in owner surveys, resulting in excessively high guidelines. The 2009 Price

Index of Operating Costs projected a 4 percent increase, and the RGB adopted a

guideline of 3 percent – a little more than enough to cover the projected

increase in expenses, given that operating costs consume less than 75 percent of

rent. But the actual increase in costs

as measured by Real Property Income and expense statements was only 0.1 percent.

In 2010 and 2011, the Price Index again greatly overestimated cost increases.

Chart 7 shows the evolution of the Price Index, rent guidelines, and RPIE costs

since 1990, clearly showing the great divergence in recent years. This divergence has resulted in higher,

unaffordable rent increases for tenants.

This is an important time for the RGB to reflect on

and revise the methodology it uses to determine what it considers reasonable

rent guideline increases. Before and since the recession struck the city, it

has tended to over-compensate owners to the expense of rent-stabilized tenants.

This is certainly a time for the RGB to exercise greater restraint by keeping

guideline increases to a minimum, for an industry that appears to be prospering

in the wake of recession. RGB should consider its unique potential contribution

to stabilizing the rental market and easing the rent-income stresses that New

Yorkers continue to experience.

Recommendations

1)

CSS urges the

New York City Rent Guidelines Board to take into account the disastrous effects

of the recession on many New Yorkers, regardless of income, and exercise overdue

restraint in setting new, minimal rent guideline increases. In past years CSS

has recommended a rent freeze; we continue to do so in light of the persistent

rent escalation that has benefited the industry in the face of a major economic

set-back for many tenants.

2)

CSS urges the

RGB to refrain from further supplemental increases at lower rent levels—what

tenant advocates refer to as the “poor tax.” RGB should do its best to minimize

increases at the low-rent levels where the poorest tenants tend to live.

APPENDIX: CSS Renter Sub-Sample

Because

of unavoidable inconsistencies and inaccuracies, in respondent reporting of

household income and contract rent, this analysis of rent burdens is based on a

sub-sample of renter households within each of the HVS samples used. The CSS

renter sub-sample for each HVS year was selected on the following basis:

1) Rent-paying households only

(exclude rent-free and owned housing)

2) Head of household age at least

25 and less than 65.

3) Households with a positive HVS

contract rent burden

4) Households within the middle

90 percent of the income distribution for renters

(excludes 5-percent outliers at either extreme) . The

resulting household income intervals used for each HVS year are as follows:

2011 $7,896 to $175,000

2008 $6,912 to $160,000

2005 $6,006 to $133,000

2002 $6,000 to $130,000

1999 $5,700 to $131,000

1996 $5,000 to $119,950

5) Households within the middle 90 percent of the contract

rent distribution for renters (excludes 5-percent outliers at either extreme.)

The resulting contract rent distributions used for each HVS year are as

follows:

2011 $342 to $2,800 monthly

2008 $252 to $2,500 monthly

2005 $208 to $2,100 monthly

2002 $200 to $1,900 monthly

1999 $177 to $1,550 monthly

1996 $163 to $1,300 monthly

6) Residual (after-rent) household income of at least $100

monthly, in 2002 dollars. For each HVS year, the residual income threshold, in

2002 dollars, was:

2011 $129

2008 $123

2005 $111

2002 $100

1999 $93

1996 $87

The

resulting CSS sub-sample can be considered a more "mainstream" sample

of New York City

Comparison: HVS and CSS Renter Samples

1996 1999 2002 2005 2008 2011

Median Income

HVS: $24,680 $27,600 $32,000 $33,904

$40,000 $40,000

CSS: $31,000 $35,000 $39,000 $40,050

$46,400 $50,000

Median Contract Rent

HVS: $ 600 $ 648 $

706 $ 850 $ 950 $1,100

CSS: $ 600 $ 650 $ 730 $

850 $ 996 $1,100

Median Contract Rent Burden

HVS: 28

% 27 % 27 % 28 %

29 % 31 %

CSS: 24

% 23 % 23 % 25 %

25 % 27 %

Percent Households with High

Burdens (50% or more)

HVS: 26

% 26 % 23 % 26 %

26 % 29 %

CSS:

12

% 12 % 12 % 14 %

15 % 18 %

1 Preliminary estimate from the U.S. Department of Labor’s Bureau of Labor Statistics.

2 We use the term “low-income” to refer to

households with incomes no greater than twice the federal poverty threshold, in

2010 about $34,114 for a family of three persons. Household incomes recorded in

each HVS are for the previous calendar year. Low-income households include the

poor, as well as the “near-poor” with incomes above poverty but no greater than

twice the poverty threshold.

3 Unemployment rates are

calculated by the Bureau of Labor Statistics from the Census Bureau’s Current

Population Survey.

5 ACS

2005-2010 data estimate renter unemployment rates of 9, 8, and 12% for 2005,

2008, and 2010 respectively, against unemployment rates of 19, 15, and 22 % for

low-income renters.

No comments:

Post a Comment